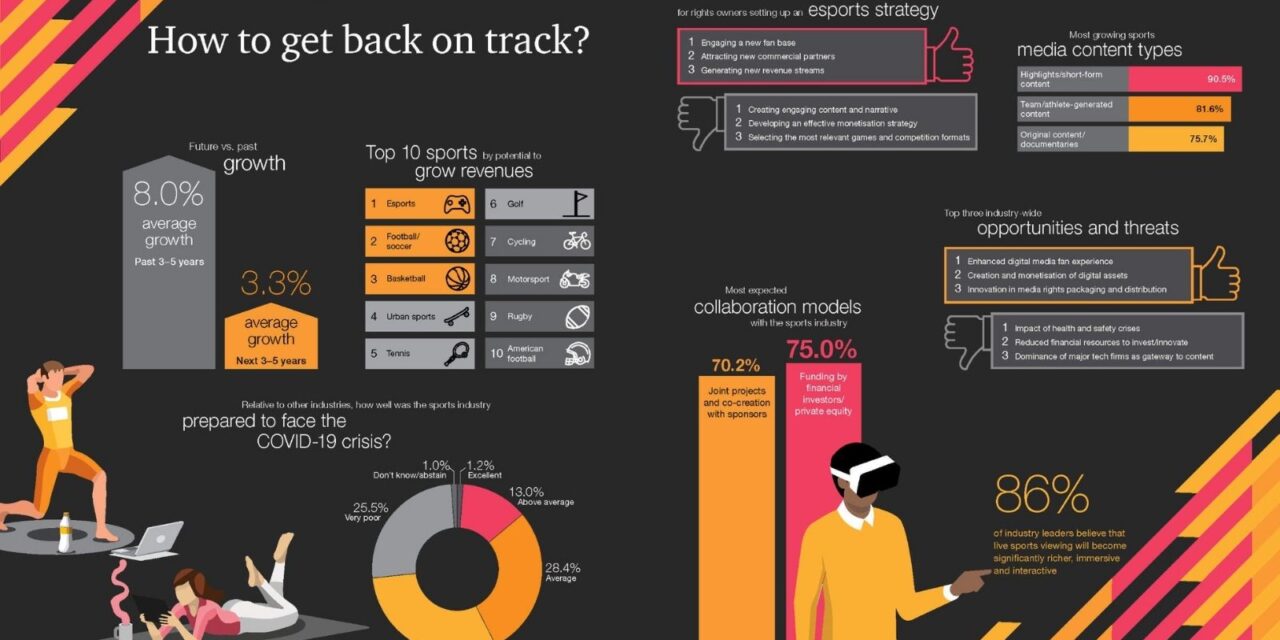

30 per cent of respondents in PwC’s Global Sports Survey expect that there will be zero growth in the sector over the next three to five years.

The overall expected growth is 3.5 per cent, down from an expected 8 per cent before the devastating impact of Covid-19.

The survey is based on input from 780 experts across 50 countries around the world. Sport for Business has been a contributor to the survey over the last number of years and we are pleased to report the findings of it here for you today.

The survey closely reviews the consequences of a crisis unprecedented in the history of modern sport.

COVID-19 undermining growth expectations

COVID-19 has strongly affected the sports market, which is expected to slow to an annual growth rate of 3.3 per cent in the next 3-5 years.

30 per cent of respondents expect the growth rate to be zero or below.

The Middle East and Asia – fuelled by robust governmental support, upcoming mega-events and overall growing commercial maturity – report the most optimistic forecasts.

Africa also anticipates steady growth thanks to an increasing influx of investments and partnerships.

In Europe, the Americas and Australasia, the crisis has significantly lowered confidence.

Esports accelerating its rise as the fastest-growing category

Benefiting from unprecedented exposure in the mainstream media, esports unsurprisingly emerged as the big winner of this lockdown period.

The simulated sports genre, which temporarily turned into a substitute for real, physical sports, is even ranked first in PwC’s yearly sports ranking.

The growth potential of the ultimate global sports – football and basketball – remains robust, as confirmed by the large broadcast audiences recorded by major competitions at the time of their respective restarts.

Interestingly, motorsport moved up to 9th place – up 5 ranks from the last edition. This may be tied to the recent experiments by flagship properties like Formula 1 and NASCAR during the hiatus, reaping great success with innovative fan engagement campaigns.

Digital strengthening its position as a major opportunity driver

Survey results show that sports leaders fully recognise the digital fan experience as a top priority, although few organisations have yet managed to deliver it in a way that allows it to acquire and retain fans sustainably.

The COVID-19 pandemic has significantly weakened physical entertainment, reinforcing the value of both immersive and interactive technologies to compensate for sports’ diminished visual and social experiences.

Health crisis squeezing resources and investments

Looking at threats, the COVID-19 crisis is unsurprisingly top of the agenda for sports leaders, with primary concerns around reduced financial resources to invest and innovate.

On the bright side, most sports leaders agree that sports’ capacity to engage audiences remains intact, as interest in the media sports product is not expected to drop.

Sports media landscape increasing in complexity

Historically, the industry has drawn its commercial value from live sports.

The pandemic has weakened this, fostering the adoption of alternative content formats and making the sports media market more complex.

As sports are being consumed in a pluralistic way, the proliferation of content buyers is contributing to forming an ecosystem that is increasingly difficult for content distributors to control.

This is the dawn of a new, convoluted reality in a market once simplified by the dominance of TV giants.

Simulated sports esports striving to keep the momentum going

The health crisis has favoured the acceleration of virtual entertainment, improving the odds for simulated sports esports.

While PwC’s analysis shows that the underlying trend is likely to continue over the long term, it should nevertheless not be taken for granted.

Sports organisations need to carry full responsibility for their esports strategy and ride the wave before other games win and lock in consumers.

“In general, our study shows that the prevailing pessimism is cut by the many opportunities brought about by the crisis. This situation may favour the emergence of changes that have long been considered but never achieved to their full extent, whether it be hybrid sports, new revenue streams, drastic governance reforms or enhanced collaborative models,” says David Dellea, Head of PwC’s Sports Business Advisory.

Starting on Monday we will take a more in-depth look at the outlook for the Global Sports Industry in the particular areas of how long the recovery might take, sports media, sponsorship, digital assets, fan engagement and more. We will also have an interview with David Dellea.